Rare Earths • PLI • China’s Rare Earth Dominance: India’s Struggle, Export Curbs & PLI Strategy

1) Why in the News

China has tightened export licensing for select rare earth elements (REEs), alloys, and magnets—critical inputs for EVs, wind turbines, electronics, and defence systems. India depends heavily on imported REE inputs, so delays or denials raise costs and uncertainty.

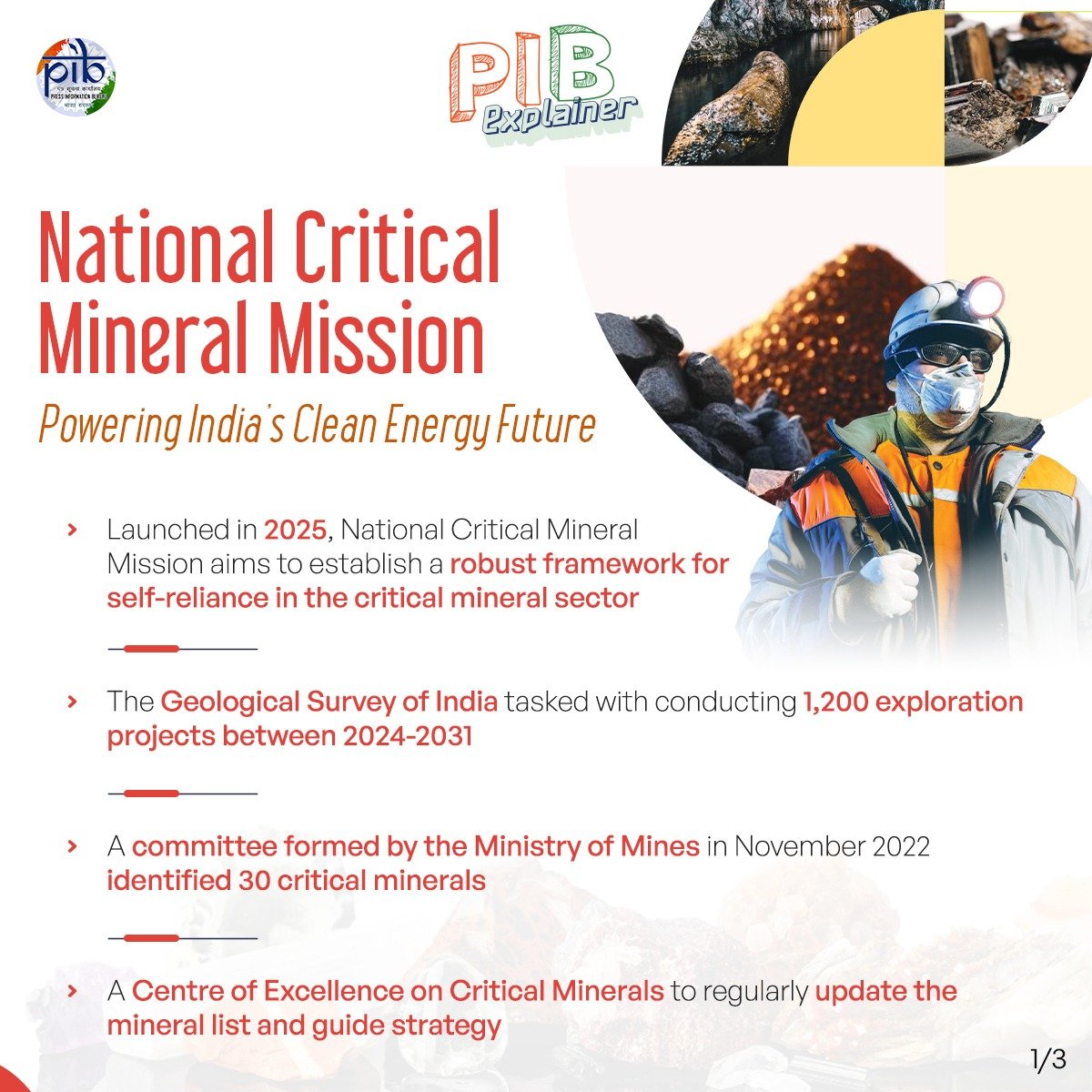

In response, India is rolling out a National Critical Minerals Mission and preparing a PLI-style scheme for rare-earth permanent magnets, while testing magnet-free EV motors as a hedge.

2) What Changed Recently—and Why It Matters

Short answer: permissions got tighter; supply chains slowed. Export licences now require end-use checks and more documentation. Shipments of REE alloys and magnets can take longer, affecting Indian manufacturers of motors, turbines, and electronics. This brings together strategic autonomy, industrial policy, technology substitution, and geo-economics.

- Export controls: Government approvals before export; they can reduce or delay shipments.

- PLI (Production-Linked Incentive): Output-based incentive to make targeted products domestically.

- Magnet-free motors: EV motors using copper coils and software control instead of rare-earth magnets.

3) Background & Core Concepts

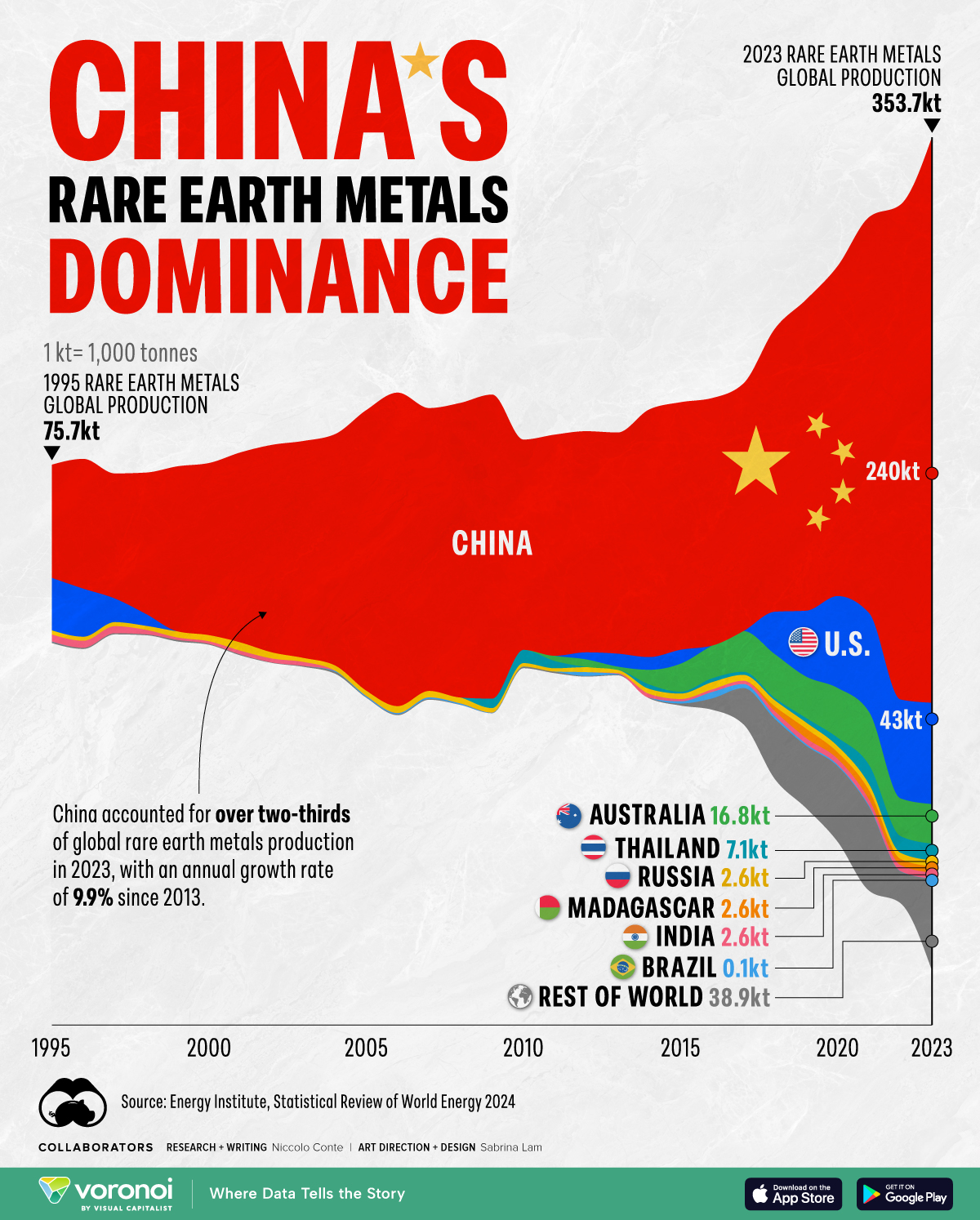

Over the last decade, China consolidated miners and built world-leading separation/refining capacity—the hardest and most value-adding stage. Globally, China produces around 70% of REE mine output and dominates processing. India has reserves (mainly monazite in beach sands) but limited separation and magnet manufacturing capability, so we import high-end inputs.

Rare earth elements (REEs) are a group of 17 metallic elements crucial to many modern technologies, from consumer electronics and clean energy to defense systems. Despite their name, most are not particularly rare in the Earth’s crust; however, they are often found in low concentrations mixed with other minerals, which makes them difficult and expensive to extract.

Key terms

- Rare earths (REEs): 17 metals crucial for magnets, electronics, catalysts, defence.

- NdFeB magnet: Neodymium-Iron-Boron permanent magnet; strongest commercial magnet used in EVs/wind.

- Monazite: REE-bearing mineral often rich in thorium; requires strict environmental and radiation safeguards.

- Separation/refining: Chemical steps to split mixed concentrates into individual oxides/metals.

- Upstream / Midstream / Downstream: Mining → separation/refining → alloys/magnets/components.

4) Where Rare Earths Are Used

- EV traction motors: NdFeB magnets enable compact, efficient, high-torque motors.

- Wind turbines: (especially direct-drive) Large magnet volumes per MW, fewer moving parts.

- Electronics & telecom: Speakers, sensors, hard-disk drives, precision polishing powders.

- Defence & aerospace: Actuators, guidance, radar, high-temperature alloys.

- Catalysts/ceramics/metallurgy: Industrial refining, glass, ceramics, specialty steels.

5) India’s Exposure & Challenges

India’s demand is rising with EVs, renewables, and electronics, but high-end materials are mostly imported.

- Limited separation capacity and almost no large-scale magnet factories.

- ESG and clearances are complex due to thorium-bearing monazite and chemical wastes.

- Technology and talent gaps in separation chemistry and magnet metallurgy.

- Price and policy volatility abroad can disrupt supplies and business plans.

- Thin recycling ecosystem, so end-of-life magnets and e-waste remain under-used sources.

6) Import Options & External Hedges

While building at home, India can diversify supply through offtake contracts and joint ventures:

- Australia and the U.S.: Established miners; growing non-China processing routes.

- Vietnam and Thailand: Emerging sources for concentrates and midstream capacity.

- Africa (e.g., Nigeria, Madagascar): Prospective deposits, but infrastructure is evolving.

- Myanmar: Potential access but high geopolitical and ethical risk.

- Reality check: Even when mining shifts, refining and magnets still lean China-centric in the near term.

7) Current Developments & Numbers

- China keeps tight control over mining quotas and export permissions for REEs and magnets.

- India has signalled incentives for domestic magnet manufacturing and recycling.

- Magnet-free EV motors are under multi-automaker trials in India to reduce dependence.

- India’s known REE reserves are significant, but output and processing remain modest.

- Global demand is driven by EV adoption and wind capacity additions, keeping markets tight.

8) Benefits & Opportunities

A full chain—from exploration → separation → magnets → recycling—can transform India’s position.

- Growth & jobs: New plants create skilled employment and supplier ecosystems.

- Inclusion & skills: Mining/coastal states gain ITI/IIT/CSIR pipelines and MSME ancillaries.

- Sustainability: Standards-based recycling reduces waste and import pressure.

- Tech resilience: Magnet-free motors and improved ferrite magnets hedge future shocks.

- National security: Lower exposure to sudden export curbs and price spikes.

9) Risks & Gaps

- Institutional coordination: Mines, Heavy Industries, Environment, and Atomic Energy must move in sync.

- ESG/regulatory burden: Radioactivity and chemical waste demand strict, costly compliance.

- Capability gap: Few domestic experts in separation and magnet metallurgy.

- Market volatility: Prices of Nd, Pr, Dy fluctuate with policy news and demand cycles.

- Geo-ethics: Conflict-zone sourcing can damage reputation and reliability.

10) Way Forward & Implementation

Overall approach: A three-track plan—(1) build at home, (2) diversify abroad, (3) back substitutes.

- Notify a focused Magnet-PLI with tiered local-value-addition and time-bound milestones.

- Fast-track separation plants via PPP/JVs; publish a model ESG code and waste benchmarks.

- Scale the Critical Minerals Mission: map deposits, auction with processing commitments, and fund pilot plants.

- Secure offtakes/equity in friendly geographies; prefer transparent, long-term contracts.

- Back substitution: Co-fund magnet-free motor pilots and ferrite-magnet R&D; align with auto and wind targets.

- National recycling network: collection targets for magnets/e-waste; end-of-life norms for wind and EV drives.

- Data & traceability: dashboard on licence delays, origin tracing, and inventory cover (weeks of demand).

- Skills & labs: Launch a Separation Chemistry & Magnet Metallurgy Mission across IITs/CSIR/NML with industry placements.

One-Line Wrap: PLI at home, diversified imports abroad, and smart substitutes together shrink China risk.

Mains Practice (answer in 150–250 words)

Q1. China’s rare-earth export licensing is a supply-chain weapon. Outline India’s strategic response.

Hints:

- Intro: Briefly note tighter licensing and India’s dependence.

- Body pillars: (i) Build domestic chain—separation → magnets → recycling; (ii) Diversify—offtakes/JVs with Australia, U.S., Vietnam, Africa; (iii) Substitute—magnet-free motors/ferrites.

- Risks: ESG/clearances, financing, skill gaps; conflict-zone sourcing.

- Way forward: Time-bound PLI, PPP separation plants with ESG best practice, recycling mandates, customs data and traceability, critical-minerals diplomacy.

- Conclusion: A three-track plan balances resilience and competitiveness.

Q2. Should India prioritise NdFeB magnet capacity or magnet-free EV motors for mineral security?

Hints:

- Intro: EVs and wind rely on NdFeB; processing is concentrated overseas.

- Body: (i) NdFeB path—highest efficiency, export potential, but capex/know-how intensive; (ii) Magnet-free path—quicker hedge using coils and control software; (iii) Dual-track reduces lock-in and buys time.

- Risks: Performance trade-offs, price swings of Nd/Pr/Dy, financing and skills.

- Way forward: Launch Magnet-PLI while funding substitute motor pilots and recycling; align with auto and wind targets.

- Conclusion: Diversification is security.

Prelims MCQs

Q1. Consider the following statement about REEs

- 1. Export licensing for rare-earth alloys and magnets can delay shipments even without a formal ban.

- 2. India already produces a large share of global rare-earth permanent magnets.

which of the above statement is/ are correct?

(a) 1 only (b) 2 only (c) Both (d) Neither

Answer

(a). Statement 2 is incorrect; India’s magnet capacity is still limited.

Q2. Consider the following statement about REEs

- 1. NdFeB magnets are used in EV traction motors and direct-drive wind turbines.

- 2. Monazite often contains thorium, which needs special handling and safeguards.

which of the above statement is/ are correct?

(a) 1 only (b) 2 only (c) Both (d) Neither

Answer

(c). Both statements are correct.

Start Yours at Ajmal IAS – with Mentorship StrategyDisciplineClarityResults that Drives Success

Your dream deserves this moment — begin it here.