1) What happened

India’s total U.S. Treasury holdings have eased to about the low-$200 billions, while overall forex reserves remain around $690+ billion.

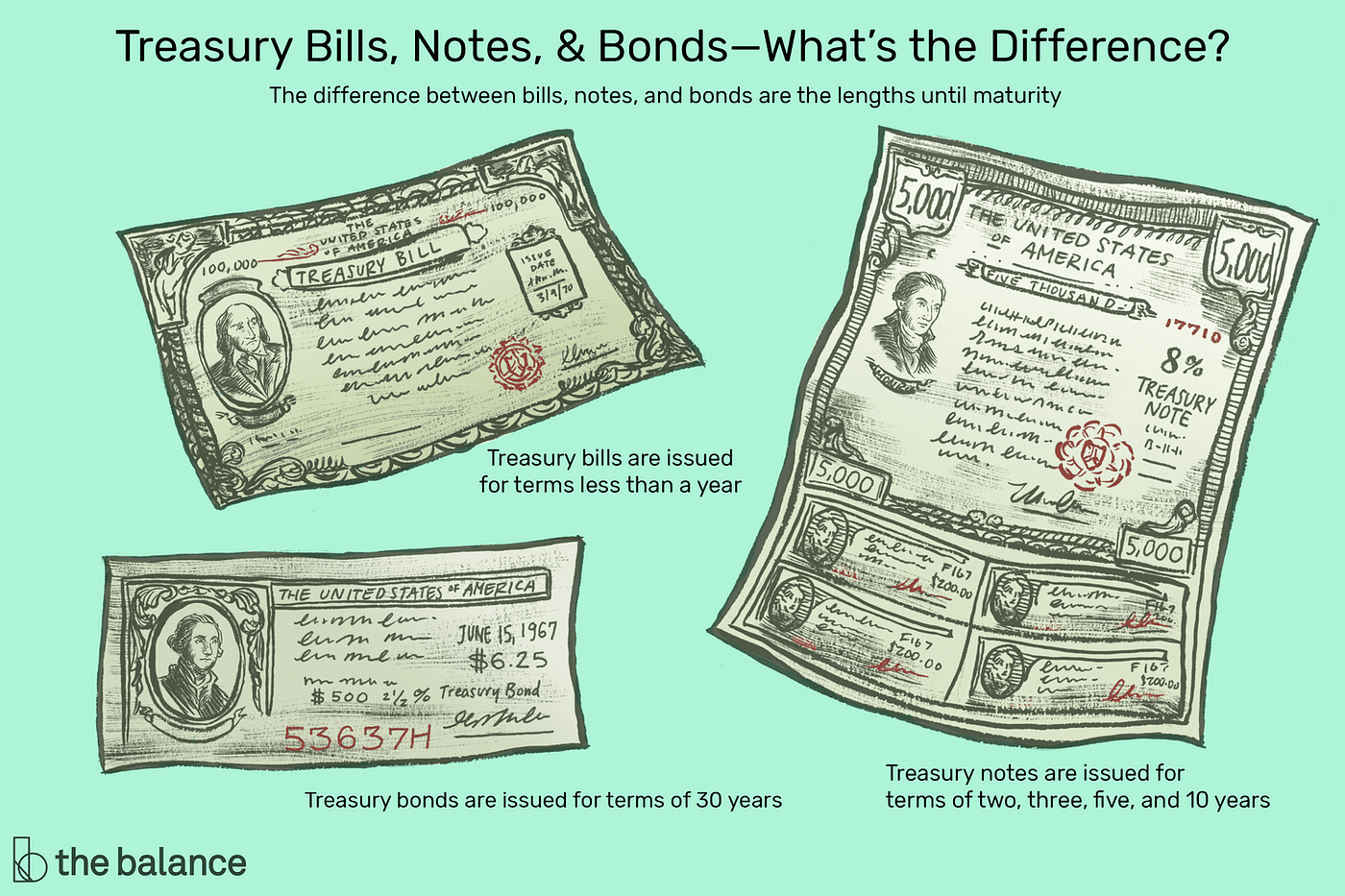

2) What exactly are Treasury Bills?

- Treasury Bills (T-bills): Short-term U.S. government securities with maturity under one year (4, 8, 13, 26, 52 weeks).

- Zero-coupon, sold at a discount: You buy below face value and get face value at maturity; the difference is the interest.

- Very liquid, very safe: Backed by the U.S. Government; easy to sell quickly.

How they differ from other Treasuries

- Notes: 2–10 years; pay coupon every six months.

- Bonds: 20–30 years; pay coupon every six months.

- Risk & return: T-bills have low interest-rate risk but usually lower yield than longer notes/bonds.

Simple example (discount math):

Face value ₹100; you buy a 26-week T-bill at ₹98.80 → at maturity you get ₹100. ₹1.20 is your interest (the annualised yield is calculated from this discount).

3) Why would RBI cut T-bills now?

- Yield view: If rate cuts are expected in the U.S., short-term yields on T-bills can fall faster. Shifting some money into longer notes/bonds can lock in today’s higher coupons and may give price gains if yields fall later.

- Liquidity vs return: T-bills maximise liquidity. If liquidity is comfortable, moving a slice to slightly longer assets can improve income.

- Diversification: RBI also balances dollar assets with euro/other currencies, gold, and supranational/agency debt to spread risk.

- Duration strategy: Adjusting the average maturity (duration) helps tune the income–risk mix.

4) Does this hurt the rupee or the economy?

No. This is normal reserve management. RBI still holds safe, liquid assets. If the new mix earns a better risk-adjusted return, RBI’s investment income improves. With high reserves and diversified assets, market confidence stays strong.

5) Key terms made easy

- Yield: Your return from a security. For T-bills, it comes from the discount to face value.

- Duration: How sensitive a bond’s price is to interest-rate changes. Longer duration → bigger price swings.

- Interest-rate risk: When rates rise, bond prices fall (and vice versa).

- Credit risk: Risk the issuer cannot pay. U.S. Treasuries have minimal credit risk.

- Liquidity: How fast you can sell at a fair price. T-bills are among the most liquid assets.

- Roll-over risk: Bills mature quickly, so you must reinvest often at the new market rate.

6) Two quick illustrations

- Discount example: Buy at ₹98.80, redeem at ₹100 → ₹1.20 interest for the period (annualised to get yield).

- Rate-cut scenario: Moving some funds from 3-month T-bills to 5-year notes before rate cuts can bring capital gains when yields fall, plus coupon income.

Prelims Practice (MCQ)

Q. With reference to U.S. Treasury Bills and central-bank reserves, which statements are correct?

- T-bills are zero-coupon securities that mature within one year.

- Moving from T-bills to 5-year notes increases portfolio duration.

- T-bills are usually less liquid than 10-year notes.

- Central banks alter reserve mix mainly to balance safety, liquidity, and return.

Choose the correct answer:

A. 1, 2 and 4 only

B. 1 and 3 only

C. 2 and 3 only

D. 1, 2, 3 and 4

Answer: A (Statement 3 is false: T-bills are typically more liquid than 10-year notes.)

One-line wrap

RBI’s move is a routine asset-mix tweak—slightly less in ultra-short T-bills, a bit more in other safe assets—to balance liquidity, yield, and risk inside India’s reserves.

Start Yours at Ajmal IAS – with Mentorship StrategyDisciplineClarityResults that Drives Success

Your dream deserves this moment — begin it here.